Author: Jessica Dickler, CNBC

Getting into college is one thing. Figuring out how to pay for it is another.

Price has become a growing consideration among students and parents. Now, financial concerns govern decision-making for nearly 8 in 10 families, according to education lender Sallie Mae, outweighing even academics when choosing a school.

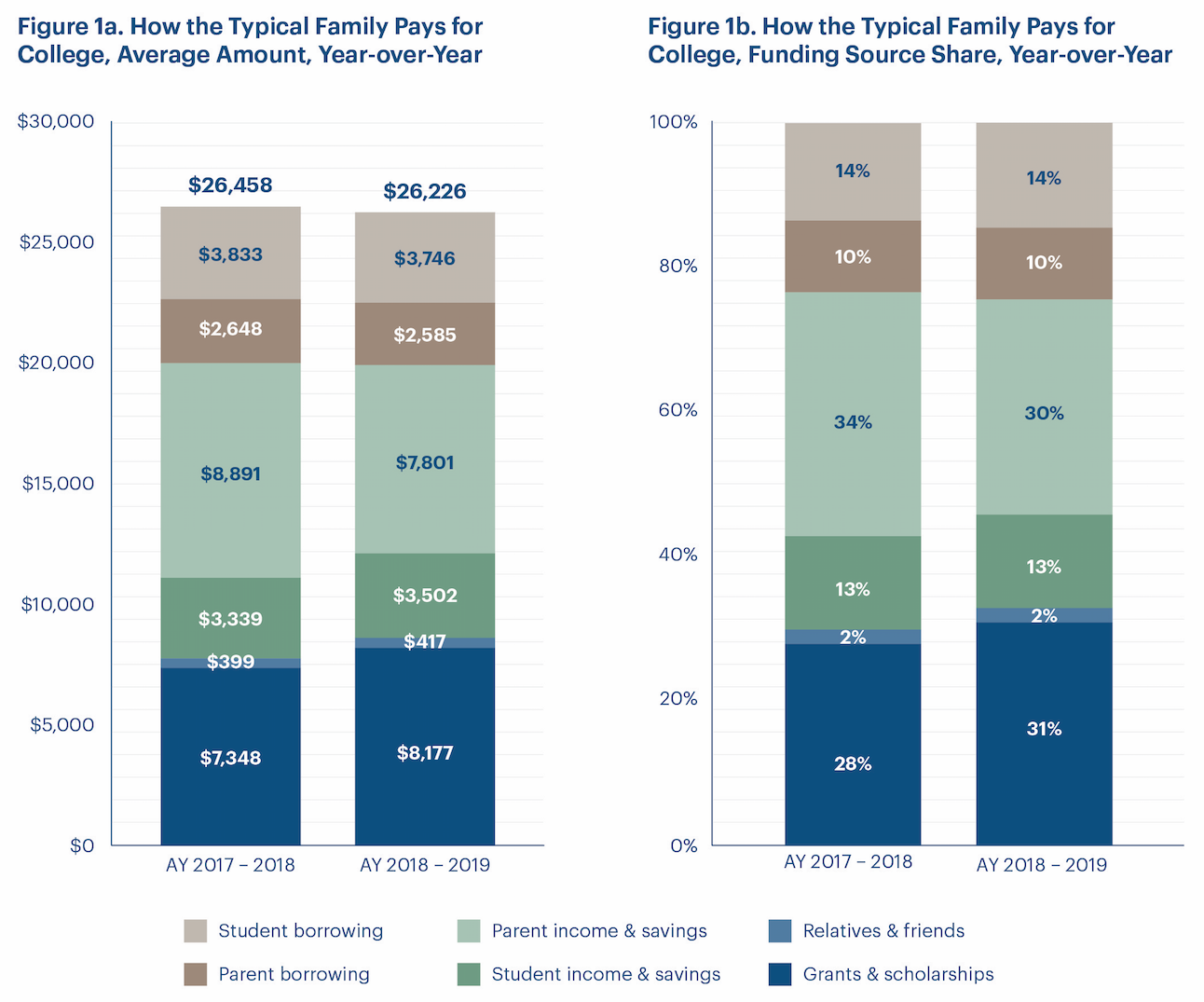

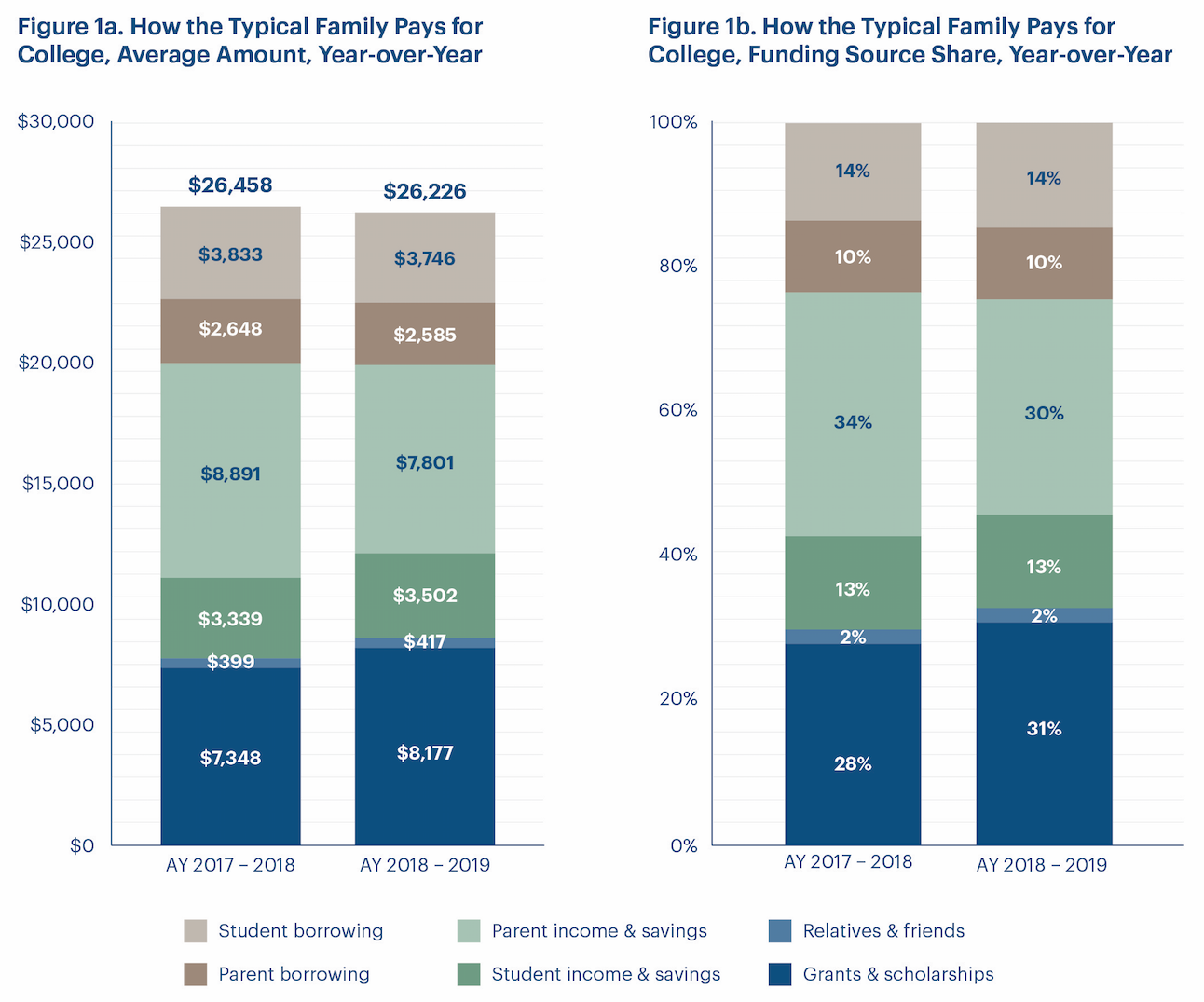

At the same time, most students and their parents pay only a fraction of the total tab, even as college costs continue to rise.

In addition to income and savings, more than 8 in 10 families tap scholarships and grants — money that does not have to be repaid — to help cover costs. More than half of families borrow, with both parents and students taking out loans, Sallie Mae found.

That’s why so much hinges on the financial aid award letter. However, it can be difficult to understand what that missive means to your bottom line.

To get a better sense of what you’ll pay out of pocket for higher education, here are the do’s and don’ts to deciphering college aid.

Don't Compare Apples To Oranges

For starters, while it may seem obvious, some schools just cost more than others. Therefore, what may look like the largest offer might not be the best.

“One school might give you $5,000 more grant aid but their cost could be $8,000 more,” said Kalman Chany, a financial aid consultant and author of the Princeton Review’s “Paying for College.”

Further, not all colleges include both direct and indirect expenses in the total “cost of attendance,” or COA, said Jennifer Satalino, a financial aid expert with Educational Credit Management Corp., a nonprofit dedicated to helping student borrowers.

While most schools outline baseline tuition and fees, some might not include “indirect expenses” such as textbooks, meals and transportation. For each school, list out all the costs, including personal expenses, Satalino said, before deducting grants or scholarships.

“You have to look at the net net,” Chany said.

Do Differentiate Free vs. Borrowed Money

In most award letters, there are often several financial aid options, including grants, scholarships, work-study opportunities and student loans.

If you’re having trouble telling the difference between gift aid and loans that will need to be repaid, look for terms like “grant,” “scholarship” and “fellowship.” Anything else is most likely a loan, Satalino said.

“If you have questions, ask — don’t make assumptions,” she added.

Even with gift aid, there may be strings attached, such as whether a grant is renewable for all four years or a minimum grade point average that must be maintained. A school that seems more generous initially might offer less funding down the road, Chany said.

If student loans are listed, they will appear to reduce the total cost of attendance. But the reality is that loans always need to be repaid — plus interest.

Don't Forget About Interest

Studies show that more than half of millennials take on student loans without knowing the interest rate or what their monthly payments will be.

Before borrowing a dime, check whether the financial aid offer includes direct loans, which are need-based and interest-free while a student is in school, or unsubsidized loans, which accrue interest from the outset. “Subsidized is always better,” Chany said.

Still, beyond differentiating between subsidized and unsubsidized loans, award letters rarely provide information about interest rates and repayment options.

If you’ll need loans to pay for college, Satalino advises that you find out the full costs of your options and then borrow only what is absolutely necessary.

Don't Take Everything That's Offered

To that end, schools will often offer more financial aid than you may need.

As a general rule of thumb, “don’t borrow any more than you estimate your first-year earnings will be” once you graduate, Satalino said.

Many people make the mistake of borrowing too much and using student loans to pay for all their expenses, and then they struggle to repay what they owe, she cautioned.

“Only take the amount of financial aid necessary to get through college,” Satalino said.